There’s an old temptation buried in every workplace, and it rarely announces itself with a bang. It shows up as a supply closet that’s never inventoried, a spreadsheet quietly adjusted after everyone else has gone home, or a company card that slowly begins to feel less like a business expense and more like a personal allowance.

Nobody wakes up one Monday and decides to become a thief. It happens one reasonable-sounding exception at a time: the “loan” from the register that was always going to be paid back, the extra hour on a timesheet that felt deserved after a brutal week, or the vendor discount quietly extended to a friend because, honestly, who would even notice?

That’s what makes employee theft so uncomfortable to study. It rarely begins with greed alone, and it rarely fits the stereotype of a career criminal slipping through the hiring process. More often, it’s committed by people who have spent years earning their employer’s trust: the bookkeeper, the office manager, or the warehouse supervisor who knows exactly which pallets never get counted twice.

Decades of occupational fraud research suggest these cases aren’t random. They tend to emerge when three conditions quietly align: pressure, opportunity, and rationalization. Remove one of them, and many schemes become far less likely.

The statistics tell the same story from a different angle. Businesses lose an estimated 5% of their annual revenue to occupational fraud. Most schemes remain hidden for about a year before anyone notices.

Nearly nine out of ten cases involve employees taking cash, inventory, or other assets, and the overwhelming majority of offenders have no previous criminal record. The numbers don’t simply measure how often theft happens. They explain why familiar patterns keep appearing across industries, organizations, and decades of research.

That’s what makes employee theft different from many other workplace risks. It’s rarely the result of a single bad hire or an isolated act of dishonesty. More often, it’s the product of ordinary people encountering ordinary opportunities inside systems that weren’t designed to catch small exceptions before they become costly habits.

The employee theft statistics below show where those opportunities arise, who is most likely to exploit them, how long they’re likely to go unnoticed, and which safeguards consistently make organizations more resistant to occupational fraud.

Why do employees steal?

Long before there’s a number to report, there’s usually a small, private calculation happening in someone’s head. Fraud examiners have a name for it: the fraud triangle, first described by criminologist Donald Cressey, and it’s held up remarkably well across nearly 70 years of case studies. It says that occupational theft tends to require three things at once – take any one away, and the risk drops sharply.

- Pressure (or motivation). Some external or personal problem that creates a felt need for money the person doesn’t have – a mortgage payment, a gambling debt, a medical bill, or simply the quiet pressure of watching peers spend more than they earn.

- Opportunity. A weakness in the system that makes theft feel achievable – no cameras, no second signature required, no one who ever double-checks the count.

- Rationalization. A story the person tells themselves so the act doesn’t feel like what it is – “I’m only borrowing it,” “they underpay me anyway,” “everyone here does something similar.”

Take away the opportunity, and pressure and rationalization mostly stay theoretical. That’s precisely why internal controls, not moral judgment, remain the most effective lever employers actually have.

A related rule of thumb, common among loss-prevention professionals, is worth knowing on its own: the 10-80-10 principle. Roughly 10% of employees will never steal under any circumstances; another 10% are actively looking for the chance; and the remaining 80% – the vast majority – will only cross the line if the right mix of pressure, opportunity, and justification happens to line up.

Most prevention strategy, in other words, aren’t really aimed at catching career criminals. It’s aimed at making sure that the middle 80% never gets the chance to find out what they’d do.

The situations that tend to supply that chance follow a fairly consistent pattern across industries:

- A sudden, unplanned financial shock – a partner’s job loss, a divorce, an eviction notice, a medical emergency not covered by insurance.

- A perceived injustice at work – being passed over for a promotion, being denied a raise that was promised, or watching a manager take credit for their effort.

- Addiction or compulsive spending, most commonly gambling, which shows up disproportionately often in the largest embezzlement cases on record.

- Status pressure – the felt need to keep pace with a peer group’s visible spending, even when the income doesn’t support it.

- A weak “tone at the top.” Employees rationalize theft far more easily in organizations where they believe leadership already cuts ethical corners, or where fraud is quietly understood to be common in the industry.

And the perpetrator profile that emerges from tens of thousands of investigated cases is, itself, one of the more counterintuitive statistics in this field: 87% of people caught committing occupational fraud are first-time offenders with no prior criminal record. Most are between 36 and 50 years old, the majority hold a university degree, and the largest single group has been with the company for six to ten years – long enough to be fully trusted, and long enough to know exactly where the gaps are.

The key numbers behind employee theft in 2026

| Metric | Figure |

| Revenue lost to occupational fraud annually | ~5% of revenue, typical organization |

| Median loss per case | $145,000 |

| Median time to detect a scheme | 12 months |

| Cases involving asset misappropriation (cash, inventory, property) | 89% of cases; median loss $120,000 |

| Cases involving financial statement fraud | 5% of cases; median loss $766,000 |

| Median loss caused by owners/executives | ~$500,000 |

| Median loss caused by managers | ~$184,000 |

| Median loss caused by rank-and-file employees | ~$60,000 |

| Fraudsters showing at least one behavioral red flag | 84% |

| Occupational fraud detected via a tip | 43% (3x any other method) |

| Tips originating from employees | 52% of all tips |

| Fraud cases resulting in criminal charges | <30% |

| Fraudsters who received no punishment after being caught | 86% (historical benchmark) |

| Share of retail inventory shrinkage attributed to employee theft | 29%–43%, depending on study/year |

Source: ACFE

A few of these numbers are worth sitting with a little longer:

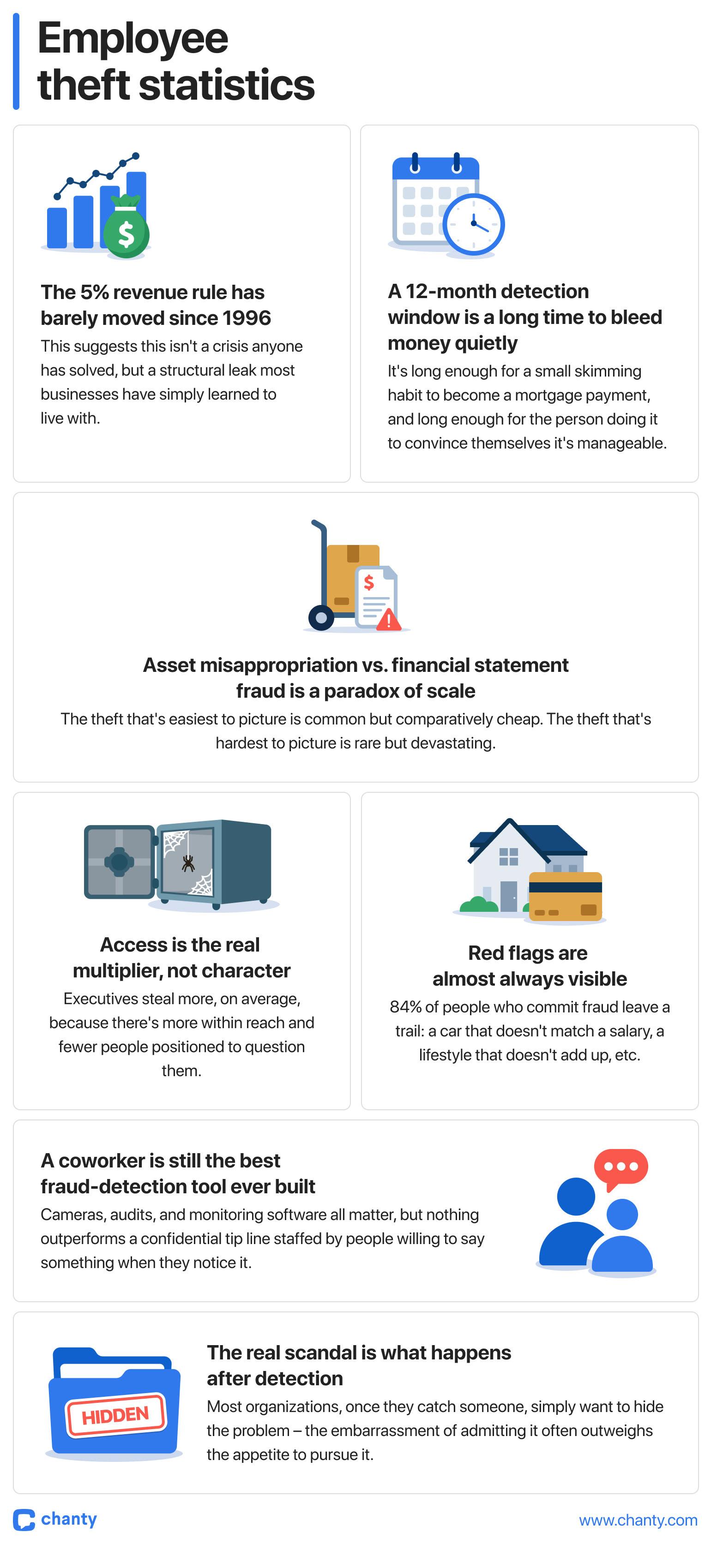

- The 5% revenue rule has barely moved since 1996. That consistency is almost more unsettling than the number itself – it suggests this isn’t a crisis anyone has solved, but a structural leak most businesses have simply learned to live with, the way an old house learns to live with a draft.

- A 12-month detection window is a long time to bleed money quietly. It’s long enough for a small skimming habit to become a mortgage payment, and long enough for the person doing it to convince themselves it’s manageable, temporary, or somehow owed to them.

- Asset misappropriation vs. financial statement fraud is a paradox of scale. The theft that’s easiest to picture – a hand in the till – is common but comparatively cheap. The theft that’s hardest to picture – a quietly falsified set of books – is rare but devastating. Most companies build their defenses against the wrong one.

- Access is the real multiplier, not character. Executives don’t steal more because they’re worse people than the employees below them; they steal more, on average, because there’s simply more within reach and fewer people positioned to question them.

- Red flags are almost always visible in hindsight. Very few people who commit fraud are quiet, disciplined criminals. Most leave a trail – a car that doesn’t match a salary, a lifestyle that doesn’t add up – and 84% show at least one of those signs before they’re caught. The signs are usually there. Almost nobody is looking for them.

- A coworker is still the best fraud-detection tool ever built. Cameras, audits, and monitoring software all matter, but nothing outperforms a confidential tip line staffed by people willing to say something when they notice it.

- The real scandal is what happens after detection. Most organizations, once they catch someone, simply want the problem to disappear – the embarrassment of admitting it happened often outweighs the appetite to pursue it. That creates a quiet recidivism risk: people who steal once and are let go without a flag often go on to work somewhere else, unreported.

How the numbers shift around the world

Occupational fraud isn’t distributed evenly across the globe, and the regional spread is useful context for any organization operating or hiring across borders. Global employee theft statistics consistently show that geography changes the size of the average case far more than it changes whether theft happens at all.

| Region | Median loss per case | Notes |

| Latin America & the Caribbean | $250,000 | Highest median loss of any region tracked |

| Asia-Pacific | $200,000 | Tied for second-highest |

| Eastern Europe & Western/Central Asia | $200,000 | Tied for second; also among the highest rates of corruption-related cases |

| United States & Canada | ~$150,000 | Largest number of cases studied overall |

| Sub-Saharan Africa | ~$154,000 | Comparable to North America |

| Western Europe | ~$150,000 | Broadly in line with the global median |

And by industry, the spread is just as wide:

| Industry | Median loss per case |

| Mining | $550,000 |

| Wholesale trade | $361,000 |

| Manufacturing | $267,000 |

| Government/public administration | $150,000 |

| Retail | $48,000 |

| Education | $50,000 |

Source: ACFE, Occupational Fraud 2026: A Report to the Nations

The pattern holds across both tables: the industries and regions with the least oversight per dollar handled – mining sites, wholesale operations, cross-border trade – tend to produce the costliest individual cases, even though they’re not always where the highest number of cases occur. Volume and severity, in other words, are two different risks, and a prevention strategy built only around frequency will miss the losses that actually hurt the most.

The situations where theft is most likely to happen

Across the industries and cases studied, a handful of conditions show up again and again as the backdrop for occupational theft:

| Risk condition | Why it matters |

| Weak or overridden internal controls | Present in more than half of all fraud cases studied, the single most common contributing factor |

| No segregation of duties | The person who can move money and the person who approves it are the same individual |

| Small organization size (under 100 employees) | Smaller companies are consistently less likely to have basic anti-fraud controls in place, leaving them more exposed per dollar of revenue |

| Long-tenured, highly trusted employees | The largest group of perpetrators had 6–10 years of tenure – long enough to know exactly where the gaps are and to be the last person suspected |

| Corruption-heavy environments | Corruption (kickbacks, bribery, conflicts of interest) appeared in 48% of all cases studied, and often overlaps with asset misappropriation |

| Absence of a confidential reporting channel | Organizations without a hotline detect fraud slower and lose roughly twice as much before they catch it |

| Sole financial oversight by owner/founder | Common in small businesses, and one of the conditions most correlated with catastrophic, undetected losses |

None of this means every long-tenured or trusted employee is a risk. It means the conditions that allow good people to slide into bad decisions are identifiable, repeatable, and – unlike character – genuinely fixable.

When the theft is horizontal: employees stealing from each other

Most employee theft statistics focus on what gets taken from the company. A quieter, less-studied version of the same behavior happens sideways, from colleague to colleague, and it’s far more common than most leadership teams assume, even if the losses rarely justify a criminal investigation. While the studies measure different workplaces and countries, they point to the same conclusion: seemingly minor theft between coworkers is surprisingly widespread.

Some of the most telling findings include:

- 10.4% of UK office workers admit stealing something from their workplace or a colleague.

- That translates to an estimated 1.6 million UK employees who have stolen directly from a coworker.

- Around 10% of office workers admit taking money from either a colleague or the office.

- 8% say they’ve taken a coworker’s laptop, phone, or another valuable device.

- One in five employees who admitted stealing from a colleague justified it by saying, “Everyone does it.”

- In the United States, 33% of workers admit stealing food from a coworker at least once.

- 47% of employees say they’ve personally been the victim of coworker food theft.

- 18% of adults admit eating someone else’s lunch from the office refrigerator.

It’s tempting to dismiss these numbers as harmless workplace annoyances. After all, nobody is calling the police over a missing yoghurt or a borrowed charger that never comes back. But the behaviour underneath them isn’t trivial. Peer-to-peer theft erodes the same thing that larger cases of occupational fraud do: trust between the people who rely on each other every day.

For HR teams, these incidents rarely arrive labeled as “theft.” They surface instead as complaints about team culture, morale, or employees no longer feeling comfortable leaving their belongings at their desks. Employee theft statistics rarely separate this category cleanly, which is one reason it remains underreported and under-addressed. It may not appear on a balance sheet, but it shows up in engagement surveys, exit interviews, and the quiet decision of a good employee to stop trusting the people around them.

When it makes the news: notable recent cases

Statistics stay abstract until you attach a face and a decade to them. In one of the largest cases to surface recently, a former chief financial officer at the Detroit Riverfront Conservancy was found to have embezzled more than $40 million over roughly ten years, quietly diverting nonprofit funds into accounts he controlled to finance a lifestyle of luxury travel and designer goods – a scheme large enough, and long enough, that it reshaped how nonprofits nationally think about financial oversight.

Around the same period, the treasurer of Arizona’s Santa Cruz County was sentenced after wiring close to $39 million in public funds to shell companies she had invented herself, using a subordinate’s login credentials to both initiate and approve the transfers – a reminder that even a two-step approval process is only as strong as the discipline behind it.

In Washington State, an assistant office manager who spent nearly a decade earning her employer’s trust used that trust to siphon $1.4 million through forged checks and personal purchases on the company card, while her own coworkers absorbed the cost through cancelled bonuses and profit-sharing. And a gaming enterprise manager for the Muscogee Nation was sentenced to prison after embezzling more than $24 million, a scheme that also involved years of falsified tax filings to keep the stolen income hidden from view.

None of these were master criminals in the cinematic sense. They were bookkeepers, managers, and finance officers – the very people organizations depend on to be the last line of defense. That’s the pattern worth sitting with: the bigger the theft, the more likely it was committed by someone who had been given the keys precisely because no one thought to ask what they’d do with them.

The legal picture, in plain terms

Employee theft usually falls into a patchwork of legal categories rather than one clean law – larceny, embezzlement, wire fraud, or breach of fiduciary duty, depending on how the money moved and who had legal control of it at the time. Embezzlement specifically requires that the person had lawful access to the funds or property to begin with, which is what separates it from ordinary theft: the crime isn’t taking something that was never yours; it’s betraying access you were given in good faith.

For employers, this creates a genuinely difficult set of decisions. Pursuing criminal charges means cooperating with investigators, sometimes for months, and often airing internal failures in the process – which is a large part of why so many cases are handled quietly through termination instead of prosecution.

Civil recovery is a separate, and usually slower, path: restitution ordered by a court is not the same as money actually recovered, and many victim organizations never see the full amount again, regardless of the sentence handed down. Employers also carry their own legal exposure here – inadequate background checks, poor separation of financial duties, or ignoring known red flags can expose a company to negligence claims from investors, insurers, or shareholders if a theft is later discovered to have been foreseeable.

None of this is legal advice, and any organization facing an actual case should be working directly with counsel – but understanding the shape of the legal terrain helps explain why theft, once discovered, is so rarely a clean, fast story.

How companies actually reduce the risk

The research is fairly consistent on what works, and it has less to do with suspicion than with structure. The same employee theft statistics that reveal where losses come from also point, fairly directly, at what stops them.

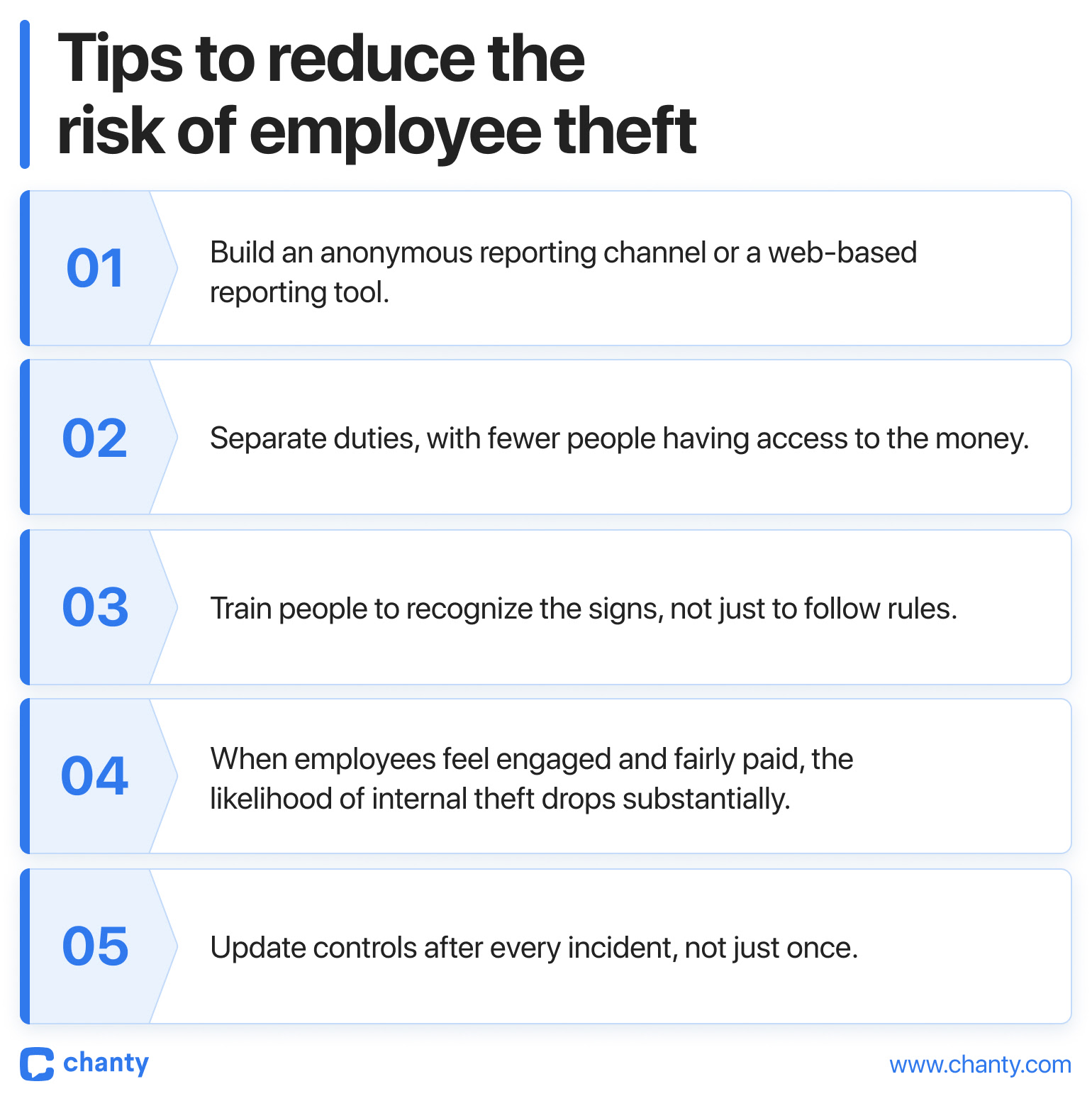

- Build a real reporting channel, and make it anonymous. Since tips catch more fraud than every other method combined, and most of those tips come from employees, a confidential hotline or web-based reporting tool isn’t a nice-to-have – it’s the single highest-leverage control an organization can put in place.

- Separate duties, especially around money. A large share of the largest cases share one detail: one person had both the ability to move money and the ability to approve that movement. Splitting those two functions between different people doesn’t eliminate temptation, but it removes the opportunity, which is usually enough.

- Train people to recognize the signs, not just to follow rules. Fraud-awareness training is associated with both smaller losses and faster detection in ACFE’s research, largely because it teaches everyone – not just auditors – what the early warning signs of financial pressure actually look like.

- Take culture as seriously as controls. Disengaged employees and workplaces where people feel undervalued or unfairly treated correlate with higher rates of internal theft. This isn’t an excuse for stealing, but it is a warning: the same conditions that drive good people to quit quietly are often the conditions that make a smaller number of people rationalize taking something on the way out. Retention and loss prevention, in other words, are closer cousins than most leadership teams assume – a workplace people actually want to stay in is also one where fewer people feel entitled to help themselves to it.

- Update controls after every incident, not just once. Organizations that revise their anti-fraud measures after discovering a theft tend to show up in the data with different loss patterns than those that don’t – a sign that most theft isn’t a one-time failure of character, but a gap in the system that, left unpatched, simply waits for the next person to find it.

After thousands of investigated cases and decades of research, one lesson keeps emerging. Employee theft is rarely the result of a single dishonest person bringing down an otherwise healthy organization. More often, it’s what happens when ordinary human behavior collides with weaknesses that nobody noticed until it was too late.

That’s encouraging in its own way. Organizations can’t eliminate financial pressure from people’s lives, and they can’t control how someone chooses to justify a dishonest decision. What they can do is reduce the opportunities that allow those decisions to become actions. Every stronger approval process, anonymous reporting channel, regular audit, and culture of accountability makes employee theft harder to commit, easier to detect, and less likely to grow into another headline or another statistic.